In 2018, Gartner predicted that 25% of Customer Service Operations would use VCA. Source: Gartner 2018.

Extract:

Analysts Present Top Predictions for Customer Experience Leaders at the Gartner Customer Experience Summit 2018 in Tokyo, February 19-20

Twenty-five percent of customer service and support operations will integrate virtual customer assistant (VCA) or chatbot technology across engagement channels by 2020, up from less than two percent in 2017, according to Gartner, Inc.

Speaking at the Gartner Customer Experience Summit in Tokyo today, Gene Alvarez, managing vice president at Gartner, said more than half of organizations have already invested in VCAs for customer service, as they realize the advantages of automated self-service, together with the ability to escalate to a human agent in complex situations.

“As more customers engage on digital channels, VCAs are being implemented for handling customer requests on websites, mobile apps, consumer messaging apps and social networks,” Mr. Alvarez said. “This is underpinned by improvements in natural-language processing, machine learning and intent-matching capabilities.”

Organizations report a reduction of up to 70 percent in call, chat and/or email inquiries after implementing a VCA, according to Gartner research. They also report increased customer satisfaction and a 33 percent saving per voice engagement.

The video in the following post shows an interaction between a VCA and a customer. The VCA’s natural way of behaving – in the video – is quite impressive. The company, Voca.ai, has since been bought by Snapchat.

As we see the surge of VCAs, we can wonder about the impact on sales people and how to best train them in this new configuration.

One of our key values is trust. We highly value this as it is the basis for a good and mutually beneficial partnership. At least, this is how we see it.

We strongly believe that the best sales people are actually “trusted advisors”. At INGAGE, our job is to train professionals in the insurance industry thanks to online courses, blended learning, virtual worlds, etc.

It’s fair to say, that that insurance industry has not always had a great reputation concerning trust, although I would argue that it has done some real improvements in the past years.

Now, when my friend Alex introduced me to the concept of “trustless” and insisted that it was very important, I was initially a bit puzzled. He actually talked about it as if it were good!

“Why would the lack of trust be good?”, I thought.

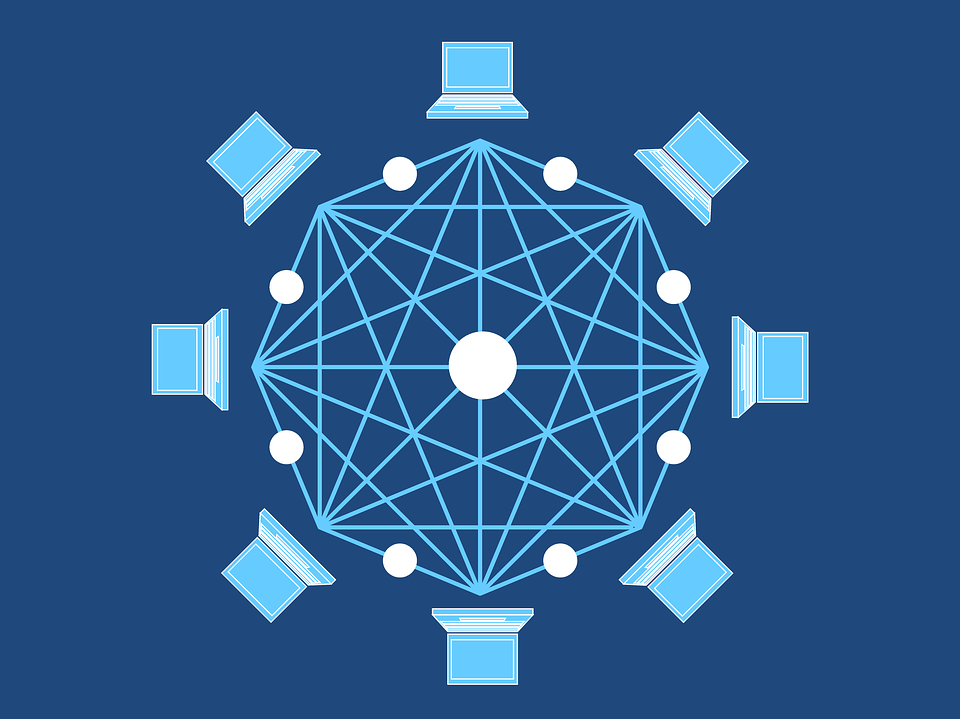

You might not often think about the system that underlies how you spend money. If you do think about it, in every transaction, there is a middleman you trust. You swipe a card, and the card processor handles the transaction, protecting both you and the merchant against fraud. You write a check, and the bank ensures you have the funds and that the other party is paid. Even paying with cash, you are using a currency monitored by a central bank, and if the cash is counterfeit, that fact will become known.

Altcoin transactions are different. You do not have to trust a third party to verify and complete your altcoin transaction. In this sense, altcoin transactions are “trustless.”

This does not mean that you should be suspicious of an altcoin transaction. In fact, the contrary is true. Why?

Let’s back up for a moment and look at the blockchain. At root, all a blockchain does is serve as a giant, public ledger. When an altcoin is mined, used as currency, or otherwise exchanged, the transaction goes on the blockchain. In order for anybody to buy and sell altcoins, their blockchains must align exactly. In other words, everybody is keeping everyone else’s books, with no central bookkeeper involved.

This is part of the system people tend to misunderstand, but it is important. Thanks to the blockchain, every altcoin transaction is recorded in a distributed ledger, meaning that it is available across multiple computers and anyone with access can see every transaction that has been recorded, all without the intervention or help of a trusted third party. You have the ledger right there in front of you, and that lets you buy and sell altcoins directly without worrying about the coins being fake. Thus, the world of altcoins is trustless, in that no middleman need be involved. You are, in effect, your own banker.

Thus, as you have understood, the fact that there is a third party that you must trust, can be an issue. The breakthrough with the blockchain is that it’s a process that ensures reliability, not a third party.

Spain is used to long working days. It’s normal for employees to start at 9 or 9.30 and finish around 20:00 – It does include a nice lunch break from 13:30 to 15:00 though. This also applies to the insurance industry there of course.

Today, I would like to speak about Liberty in Spain. As you know, Liberty is a traditional US insurance company. Not exactly a startup! They have a very long-standing experience in the industry and could be considered quite conservative.

Now, things might be on their way to change. Indeed, Liberty Seguros (Liberty in Spain) will allow its 2,000 employees in Europe to telecommute permanently. They are investing heavily on technology to adapt to the new normal and improve their employee’s experience. This will allow their workforce to become ‘digital nomads’ around Spain. You can expect to hear about engagement and training platforms that they will be deploying to address their new needs.

However, some senior managers around the world still doubt the remote working model. It is a great model, but it is not for everyone.

At INGAGE, we have been a ‘digital-first’ company from the start. It is in our DNA. We help our clients digitize their training, their academies. We address their needs to generate content in a very dynamic way that will be available on demand for their employees, clients and salesforce. We look forward to seeing Liberty Spain’s result at the end of the year.

You may have heard a lot about topics on how to make tourists love your country more. But today I’ll talk about something different, which is, how tourists help ‘me’ to love my country more?

A new trend is rising in tourism

We are witnessing a change in tourism trends – mass tourism vs slow tourism (e.g. digital nomad type of tourism). In Croatia, island hopping was very popular for the last few years. Tourists would land in Split and spend one to two days in each city or island till they reached Dubrovnik. Their holidays would pass very hectically and be rich in touristic content. Now with rising security measures, it is more complicated to travel so you cherish your time at each location even more. When you stay at one place long enough to start recognizing local people, when you find your favourite spot on the beach or best spot for coffee, you begin to identify with your destination.

Now you see how mass tourism has had a bad influence – bringing mostly consumers and a lot of pressure on the environment. That said, the new trend of tourists who stay longer in one place – that is their ‘’home’’ for the moment – goes hand in hand with rethinking the responsibility we all have to make our home sustainable for generations of local and tourists to come.

The positive aspects of the new trend

My perception of tourism is dual: the first point of view is as a small business owner who depends on tourism and its economy; the second point of view is as a landscape architect, looking out for the preservation of our natural resources and saving small-town identity – ”Genius loci”.

I feel that I have insider info from both sides that can actually be used for changes on a small-scale along with long-term big effectivity.

I’m living partly in Split now, a small Dalmatian town that had experienced a touristic boom over the last few years. That makes me feel partly like a tourist in my own country. With COVID, Split has become a go-to place for Digital nomads from all over the world and some of them I befriended. And that inspired me for this post.

They come mainly because of the weather, with the sea nearby, sunshine, feeling of safety, you can spend most of the days doing outdoor activity. So they do, Digital nomads hang out and organize group yoga, language exchange, and hiking trips. But what truly amazed me was their local actions that they are willing to participate and even organize – from beach cleaning, helping out people who lost their homes in the earthquake, volunteering in animal shelter…they give us an objective view of our daily surroundings that we are used and numbed to.

How can we continue the virtuous cycle

Digital nomads give us the momentum to act towards making our home inviting to people who will come as a responsible individual, a sustainable tourist. The one who will immerse in our laid back culture and richen our daily lives.

They are leaving us with understanding what makes us special. We should use their wide travel experience to treat our home with respect and grow it with the guidelines below:

Invest in an open, transparent community where people can engage, they want to but don’t know how to

Use ecological principles in daily lives and be proud of it. Reuse! Repurpose! Respect natural surroundings!

Walk, bike – take care of your own body, it will bring you satisfaction and you will actually see the places in your hometown they love the most and you haven’t seen in years.

Support local small food producers – help them, talk to them, find out their story and be proud to make friends with them -then recommend them to your tourist – they will be very happy and feel included.

Following just these little steps, you will see your community with different eyes – it will have a new social layer and enrich your life so you can be proud to be part of the positive change tourism will bring us. It actually already has!

Bootstrapping is one of the strongest forms of entrepreneurship, meaning start and proceed a business without external capitals. They will survive through very little money and no outside investments to build their business.

That makes the very difference between bootstrapped start-ups and fund-raised companies. Bootstrapped businesses expect to have slow and quiet growth, focusing on business models to offset the costs. On the other hand, companies involved with external funding or help will be expected to have a higher growth rate so that they could strategically meet the investor’s ROI.

Many of the successful companies had their beginnings as a bootstrapped company. Including,

Dell Computers

Facebook Inc.

Apple Inc.

Coca Cola Co.

In this article, I will write about bootstrapping in business, financing methods, stages and pros and cons of bootstrapping.

Bootstrapping Financing methods

Owner Financing: The use of personal income and savings.

Personal Debt: Credit card debt, personal loans

Sweat Equity: A party’s contribution to the company in the form of effort.

Minimize Operating Costs: Keep costs as low as possible.

Inventory Minimization: Requires a fast turnaround of inventory.

Subsidy Finance: Government cash payments or tax reductions.

Selling: Cash to run the business comes from sales.

Bootstrapping process

Early Stage The entrepreneur utilizes personal savings or borrowed or investment money from friends and family. Also, the founder mightberunning or working for other projects.

Customer and (or) Sales-Funded Stage In this stage, money from customers is used to keepthe business operating and, eventually, funds growth. Once expenses are met, growth will speed up.

Credit Stage In the credit stage, the entrepreneur must focus on the funding of specific activities, such as improving equipment, hiring staff, etc. At this stage, the company takes out loans or may even find venture capital, for expansion.

Companies Eligible for Bootstrapping

Early-stage companies They do not need a large amount of capital which will allow for flexibility for the business and time to grow.

Serial entrepreneur companies The founder has capital from the exit of previous companies they can use to invest could reap the benefits of bootstrapping

Advantages of Bootstrapping

Full control Founders will hold total control over the finances which allows themto maintain control over the organization’s cash flow. Equity is retained by the owner and can be redistributed at their discretion. This can ensure that the business is moving in the direction desired, according to the founders’ vision and cultural values, without any external influence, and when successful, keeping the profits for themselves.

Low barriers of entry Start with the founder’s own money means that super-efficiency is necessary. Solving problems without external funding means that bootstrappers have to become resourceful and develop a versatile skill set.

Focus on the business itself Raising external finance can be a very stressful and time-consuming task. By bootstrapping their company, founders can concentrate on the core aspects of the business such as sales and product. Additionally, due to the limited cash supply, it’s normal to have alternative options such as factoring, asset re-financing, and trade finance with bootstrapping.

Disadvantages of Bootstrapping

Personal liability – High risk of failure All financial risks pertaining to the business in question all fall on the owner’s shoulders. The owner is forced to put either their own or their family/friend’s investments in jeopardy in the event of the business failing. The founder needs to become adept at handling stressful situations that might crop up if you finance your company using debt to another person, such as family members and friends. Understanding what is expected and communicating this clearly to others can help you cope with the stress of the situation.

Limited cash flow Without the aid of occasional external sources of funding, entrepreneurs can find themselves unable to promote employees or even expand their businesses. A lack of money could possibly lead to a reduction in the quality of the service or product. One reason some bootstrapped companies are unsuccessful is due to the lack of revenue: Profit may not be sufficient to meet all costs.

Starting a business most often requires very long hours of work just to keep your business going, plus, usually, there is no stipend to go with this effort. All problems are yours, as hiring staff is not usually an option.

Bright side

Building your own financial foundations is a huge attraction to future investors. Investorsare much more confident when it comes to funding businesses that are already backed and have shown promise. Flaws can be corrected with growth, such as product and service. Therefore, perfection at the launch of the business is not a necessity.

The Insurance Day took place in Argentina this year on May 22.

The key topic were digitization, disruption, Artificial Intelligence and Big Data.

As the behavioural economist Dan Ariely once tweeted, “Big data is like teenage sex: everyone talks about it, nobody really knows how to do it, everyone thinks everyone else is doing it, so everyone claims they are doing it.”

“22% of insurance, asset and wealth management business is at risk to disruption from FinTechs according to our Global FinTech survey. Almost three quarters of insurance leader surveyed in the survey considered that insurance would be the most disrupted industry. Meanwhile, complex processes with multiple interactions, duplication of data entry and risk of fraud slows down traditional players’ ability to react.” PwC

Insurance companies are very much aware of the FinTech revolution: 74% of respondents see FinTech innovations as a challenge for their industry. There is a good reason to believe that insurance is indeed heading down the path of disruptive innovation, whether it is the effect of an external factor, such as the rise of the sharing economy, or the ability to improve operations using artificial intelligence.

However, despite these emerging trends, a disconnect exists between the amount of disruption perceived and insurers’ willingness to invest to defend against and/or take advantage of the innovation: 43% of the industry players claim they have FinTech at the heart of their corporate strategies, but only 28% explore partnerships with FinTech companies and even less than 14% actively participate in ventures and/or incubator programs.

Incumbent insurers who are currently focused on catching up with their competitors around customer centricity and other current trends are missing the opportunity to become proactive. They need to create a clear and consistent message that will demonstrate their willingness to play in the new InsurTech space and act accordingly – only such an approach will position incumbents to be frontrunners in the new insurance era.